Boosting Your retirement: the major updates to the secure act 2.0

The SECURE Act 2.0, also known as the “Furthering and Improving Retirement Security” Act, was recently passed as part of a fiscal omnibus federal spending bill. This legislation includes several changes to the rules around required minimum distributions (RMDs) for retirement accounts.

For a bit of background, retirement accounts are given tax advantages, either tax-deferred growth or tax-free growth in the case of a Roth account. However, the government wants people to eventually spend these accounts to fund retirement, so it established rules for mandatory beginning dates for RMDs. The previous law set the age of 70 1/2 as the general starting point for RMDs, however, the SECURE Act in 2019 pushed out the required beginning date to 72.

Now, with the passing of the SECURE Act 2.0, RMD changes are again looming large. Let’s take a look at five provisions that will impact RMDs moving forward as part of this new legislation:

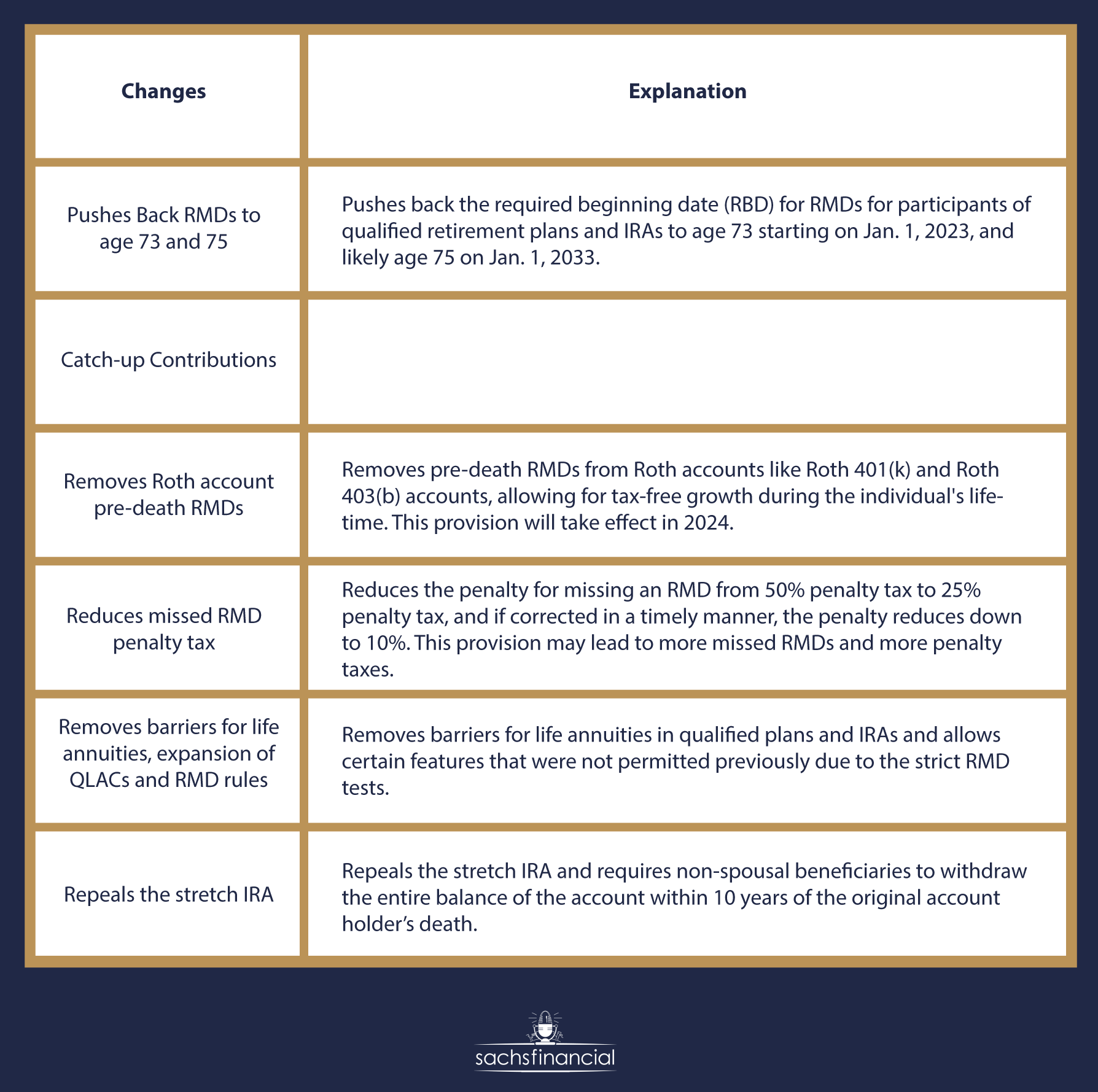

- Pushes back RMDs to age 73 and then 75:

The SECURE Act 2.0 pushes back the required beginning date (RBD) for RMDs for participants of qualified retirement plans and IRAs. Starting on Jan. 1, 2023, the RBD will move from age 72 to age 73. However, anyone who already turned age 72 by the end of 2022 will still be subject to age 72 RBD. Additionally, the age likely increases to age 75 on January 1, 2033, however, there is currently a drafting typo in the bill that will likely be resolved in the future. - Catch-up contributions:

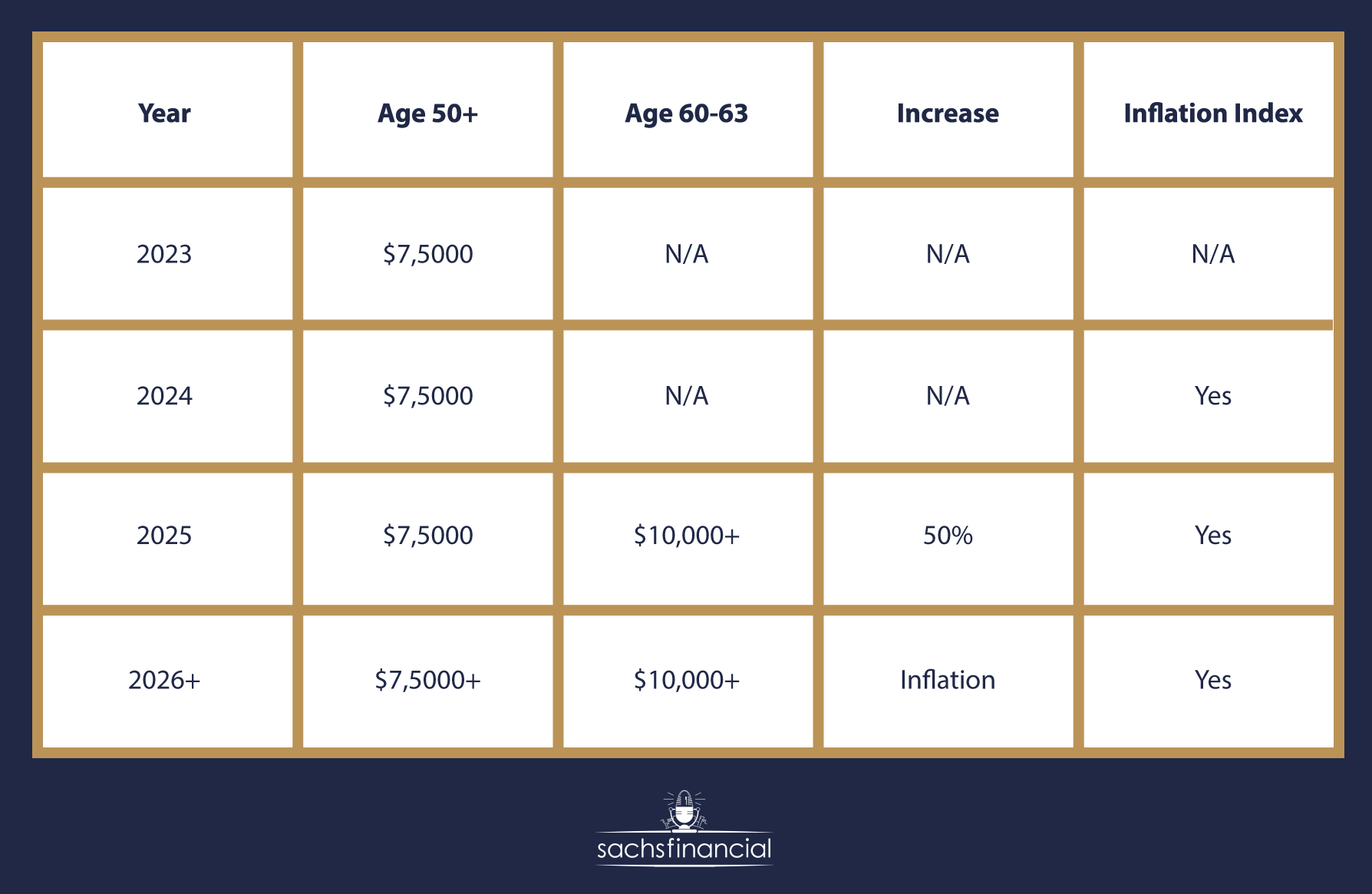

In 2023, individuals over the age of 50 will be able to make catch-up contributions of up to $7,500 to their retirement plan. Starting in 2025, the catch-up contribution limit for those between the ages of 60 and 63 will increase to either $10,000 or 50% more than the regular catch-up contribution limit in 2024, whichever is greater. Catch-up contributions will be adjusted for inflation each year after 2025.

- Removes Roth account pre-death RMDs:

The SECURE Act 2.0 removes pre-death RMDs from Roth accounts, like Roth 401(k) and Roth 403(b) accounts. Under current law, Roth IRAs are not subject to RMDs while the owner is alive, but Roth 401(k) and 403(b) accounts are subject to RMDs pre-death. This provision will take effect in 2024. - Reduction of missed RMD penalty tax:

The SECURE Act 2.0 reduces the penalty for missing an RMD from a 50% penalty tax to a 25% penalty tax. Additionally, if the RMD is corrected in a timely manner, it would reduce the penalty again down to 10%. This provision may lead to more missed RMDs and more penalty taxes, as the IRS may enforce penalties more frequently with potentially increased funding and scrutiny. - Removes barriers for life annuities, expansion of QLACs, and RMD rules:

The SECURE Act 2.0 removes barriers for life annuities in qualified plans and IRAs, and allows certain features that were not permitted previously due to the strict RMD tests. This change would allow annuities to offer an increasing payment if the payment is at least a “constant percentage” increase annually, and no more than 5% increase a year. Additionally, the changes would allow someone to choose a lifetime income annuity with a return-of-premium-at-deathbenefit and still meet the RMD rules. - Repeals the stretch IRA:

The Secure Act 2.0 also repeals the stretch IRA and requires non-spousal beneficiaries to withdraw the entire balance of the account within 10 years of the original account holder’s death.

In summary, the SECURE Act 2.0 brings a number of changes to the rules around required minimum distributions (RMDs) for retirement accounts. Some of the most significant changes include pushing back the RBD for RMDs to age 73 and then 75, removing pre-death RMDs from Roth accounts, reducing the penalty for missing an RMD, removing barriers for life annuities in qualified plans and IRAs, and repealing the stretch IRA. These changes provide more flexibility and control for individuals managing their retirement savings, as well as increased accessibility and security for retirees. It is important to note that these changes could have an impact on retirement planning and should be considered when making decisions about your retirement savings.

We are here to help—give us a call and we can discuss all of these changes and how they might change your retirement plan or affect your future planning decisions.