maximize your social security benefits

maximize your benefits

Social Security can be one of the most confusing parts of retirement. Especially when it comes to your income. One of the best things you can do to help your future retirement income is to maximizing your Social Security benefits. This will forever increase your retirement “paycheck” without relying on your investments. Unlike investment portfolios, dividends, or market gains, Social Security is a retirement income that guarantees payments for life. An annuity payment backed by the full faith and credit of the United States government.

The short answer is no one knows. However, life expectancy tables show we are living longer. We may need to prepare for 30 or more years living in retirement. Data pulled from a retirement trend study shows on average married couples over the age of 65, have more than 20% living past 90. Naturally, question arise with our clients: How can you prepare for a long retirement? Where and how will you have a monthly paycheck? In some cases, phasing out working by working for a few more years (aka a partial retirement) might be the answer.

In some cases, if you are married, deferring one of your social security payments will help your future income. Or discuss with your advisor if having the higher wage earner delay benefits is right for you.

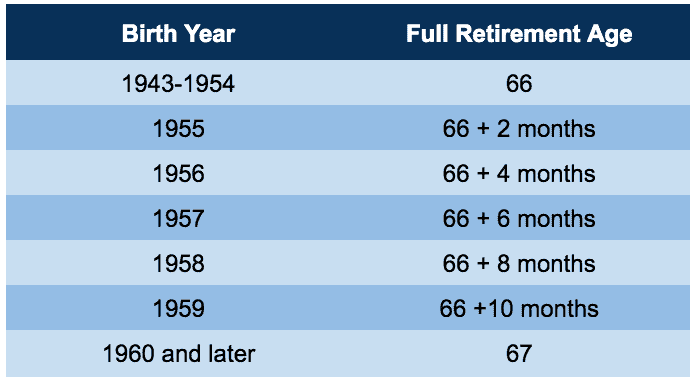

when to file

How do you know what strategy is the right one? Which way do you file? These are just two of the many questions an advisor who knows social security strategies can help you maximize your benefits and increase your lifetime income. Today, knowing when to start collecting social security benefits is anything but simple.

When we talk with you, ask us for an analysis on all your options. As part of a plan, we can help you figure out how to truly maximize your benefit. This is one of the only pensions many retirees have to rely on. The successfulness of a retirement plan can hinge on when and how to take your benefit.

This is the hardest part of retirement. What are your goals and how can we achieve them? The focus we place on retirement planning fluctuates during our lifetime.

As a young post-grad adult, someone entering the workforce, you are focused on other things than retirement. You are currently think about starting a family, paying of debts, buying a home. And maybe the last goal is to save for the future retirement. Generally you will start contributing to your work plan: 401(k), 403(b), TSP, TSA, etc.

Now you have been working for a few years. The focus shifts to saving for retirement. Now is the time you think about setting specific income and asset targets. At this point you might also talk with an advisor. The sooner you start saving the better your retirement plan will be, the more private pensions we can establish. And the less we will need to rely of social security. Saving early in your plans at work will help with future planning. But it is a hard thing for some of us to do.

Here we are 10ish years away from retirement. Now we are focused on preserving what you have built. Over the last 80-90,000 hours of working you have become an expert on accumulating retirement funds. The planning early on has hopefully helped you plan for the next phase.

It’s here at last. We are reaching the retirement age. Now we need to shift our thinking from accumulating to what we call the “distribution phase”. Instead of deferring your income, we now taking funds out to create the paychecks we need.

Does the number really matter? Your retirement planning starts long before you retire, and, the sooner the better. But, lots of experts tell you that you need a specific “magic number,”. This is the income you need to retire comfortably. No one person or couple’s is the same.

Previously, many advisers would recommend that you need around $1 million to retire comfortably. However, we do not believe in any one number for everyone. Afterall, you do not live on your assets, but the smaller monthly paychecks they will create. A different way to think about this is to define success.

Success in retirement is creating efficiency with your money. Let’s figure out what you need your retirement to do, what you want your retirement to do, and make it happen. Don’t spend time focusing on the number to hit, but on creating ways to maximize your income you cannot outlive.

If you are stuck on the number, you can try to apply “rules of thumb” to give you an idea of how much to save. A good approximation is to use the 80% rule. Plan on needing about 80% of your working income during retirement. For example, if you made $100,000 per year, then you would need savings that could produce $80,000 per year for roughly 20 years, or a total of $1.6 million. These numbers can be daunting, so in our office we focus on creating the paychecks that you can live on for your lifetime.

We believe that a good social security plan start with knowing your needs. What does it cost to be you, how much do you spend, and what do you want to do in retirement? Once we know the answers to these questions, a plan can take shape. It should be a good mix of accumulated assets PLUS “private pension” and SSI benefits. Today, less than 13% of people have access to an employee sponsored pension. If you don’t receive one from your employer, using your saving to fill any income gap may help you maximize your social security.

Starting your social security payments may cause you to miss out on up to 30% of the monthly payment you’d be entitled to at your full retirement age. But, there is a strategy that relies on just that, starting early. If you have worked long enough to qualify for benefits, you can start taking benefits as early as 62. And the “start, stop, start” strategy is aimed to help you get a jump start on your retirement.

“Give the best eight years of your retirement to yourself instead of your employer.”

The concept was coined by expert Larry Kotlikoff, an economics professor at Boston University. He found a way to use the rules and laws that make social security complicated, and find a way to help you retire early. The question to ask yourself is when will you be healthier… In your 60s or your 70s? And if you are able to, why not give the better years to you rather than your employer?

If you are ready to retire at 62, and you qualify, lets turn on your benefits early. Using this time to create other sources of income. Step 2 is to turn off your income payments at your FRA. As discussed you will receive deferred interest credits and cost of living adjustments (COLA). Once you reach full retirement age (70 years) we turn on your benefits again, at a higher level. Behind the scene your benefits will grow 8% each of the years you postpone taking them until you reach age 70.

A voluntary suspension is for retirement benefits only. There is no such provision for family and survivor benefits. As long as your retirement benefits are suspended, your spouse and children cannot collect family benefits from you. Similarly, spousal benefits you might take are also suspended. And if you have not yet reached full retirement age, the only option for stopping Social Security payments after a year of receiving them is to apply for a “withdrawal of benefits,” a more formal process that, unlike a suspension, requires you to repay Social Security the benefits you have received to date.